April 29, 2026

The summer shopping season begins weeks before Memorial Day, and this year even earlier as small decisions about what to keep, what to cut, and what to prioritize are already showing up in shopping behavior.

Drawing on Ibotta receipt data across millions of purchases, a pattern emerges: rather than uniformly pulling back, many shoppers appear to be reallocating. Spend is moving away from convenience and discretionary categories and toward staples and at-home consumption.

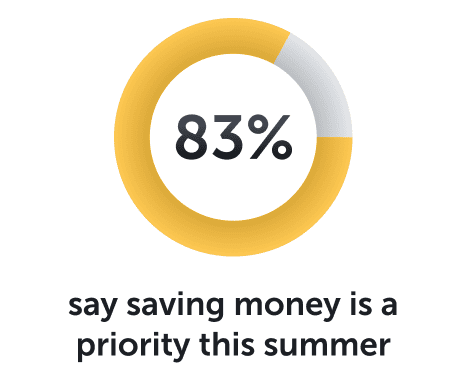

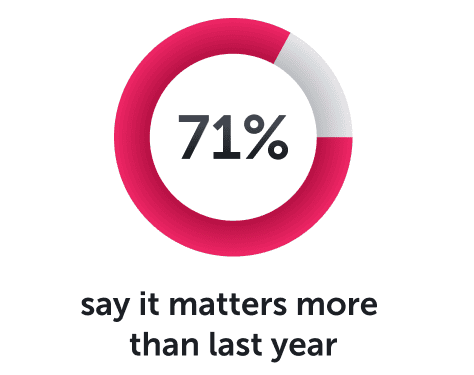

Additionally, Ibotta surveyed 500 consumers about their plans heading into summer 2026. The results confirm the purchase trends and point to a season of barbecues and stay-cations rather than dining out and summer trips.

A value-driven summer is taking shape

Since February, gas prices have risen 25.1%, and 20.9% of shoppers report cutting grocery spend to offset those costs. The pressure is showing up quickly: following the early March price spike, nearly every tracked CPG category posted week-over-week declines.

But shoppers do not appear to be abandoning spend. Basket sizes remain relatively stable. What’s shifting is composition: Staples hold while discretionary and convenience categories are absorbing the pressure.

That same pattern shows up in forward-looking sentiments from the consumers we surveyed. This reflects a continued shift toward more deliberate shopping.

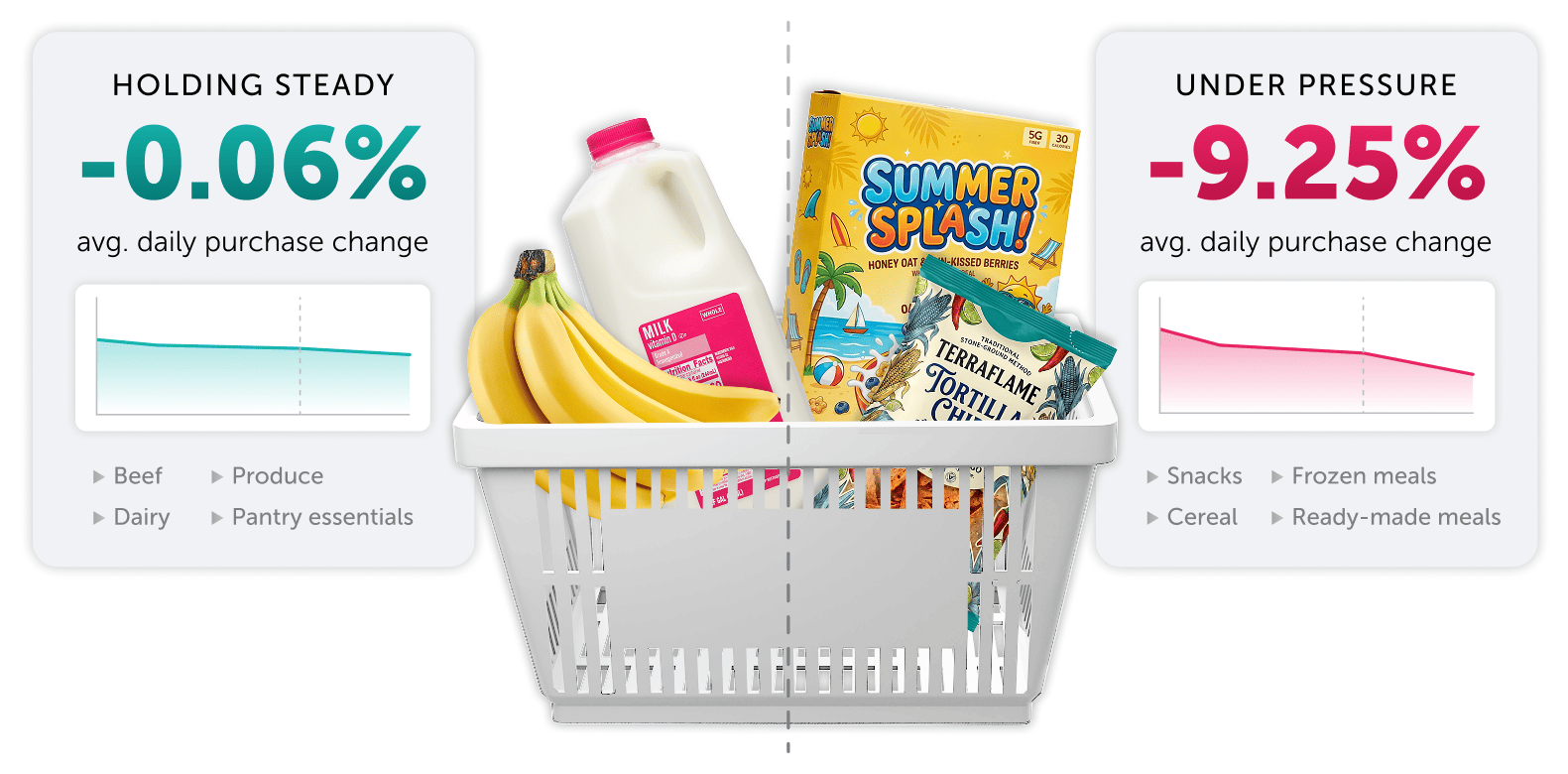

The basket tells the story: Stability vs. softness

Category-level data reinforces this trend. Staple categories like beef, produce, dairy, and pantry essentials have remained relatively flat (-0.06% in daily purchases).

By contrast, convenience-driven categories are not. Frozen meals and snacks, cereal, and refrigerated ready-made meals are down an average of -9.25% in daily purchases.

Even seasonal demand appears to be moderating. Easter-related categories saw an average 8.5% year-over-year decline in daily sales, suggesting that the holiday lift is no longer a given.

This divergence suggests shoppers are not broadly reducing consumption so much as prioritizing control. Items that support planned, cost-efficient meals are holding, while items associated with impulse, convenience, or premium pricing are more exposed.

From travel to stay-cation

Two-thirds of shoppers still plan to travel this summer, but nearly a third expect to take fewer trips. Cost is the dominant factor, cited by 68% of those pulling back.

In many cases, those dollars appear to be moving elsewhere.

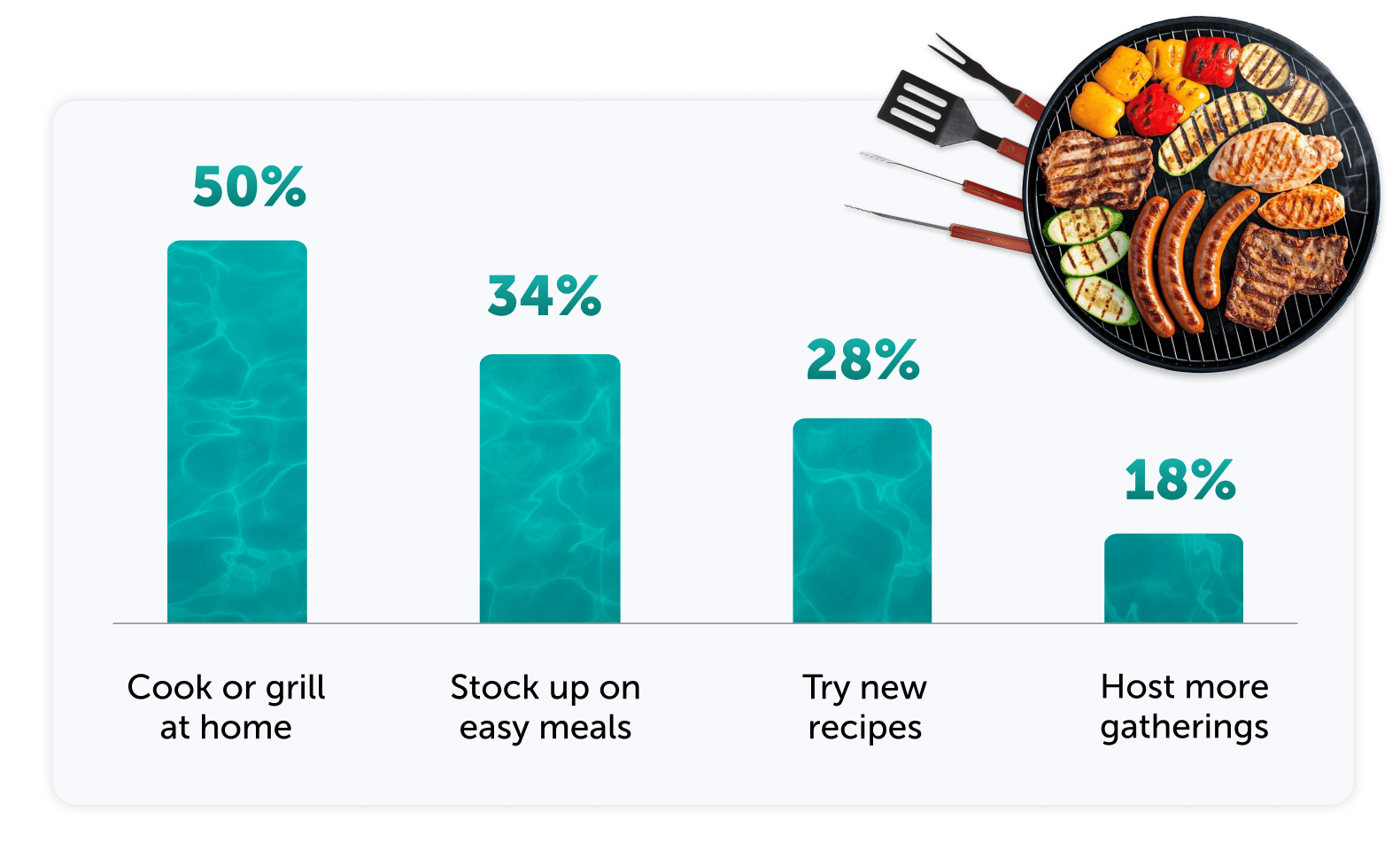

At-home activity: What shoppers plan to do instead of travel

This suggests that reduced travel may translate to increased at-home consumption.

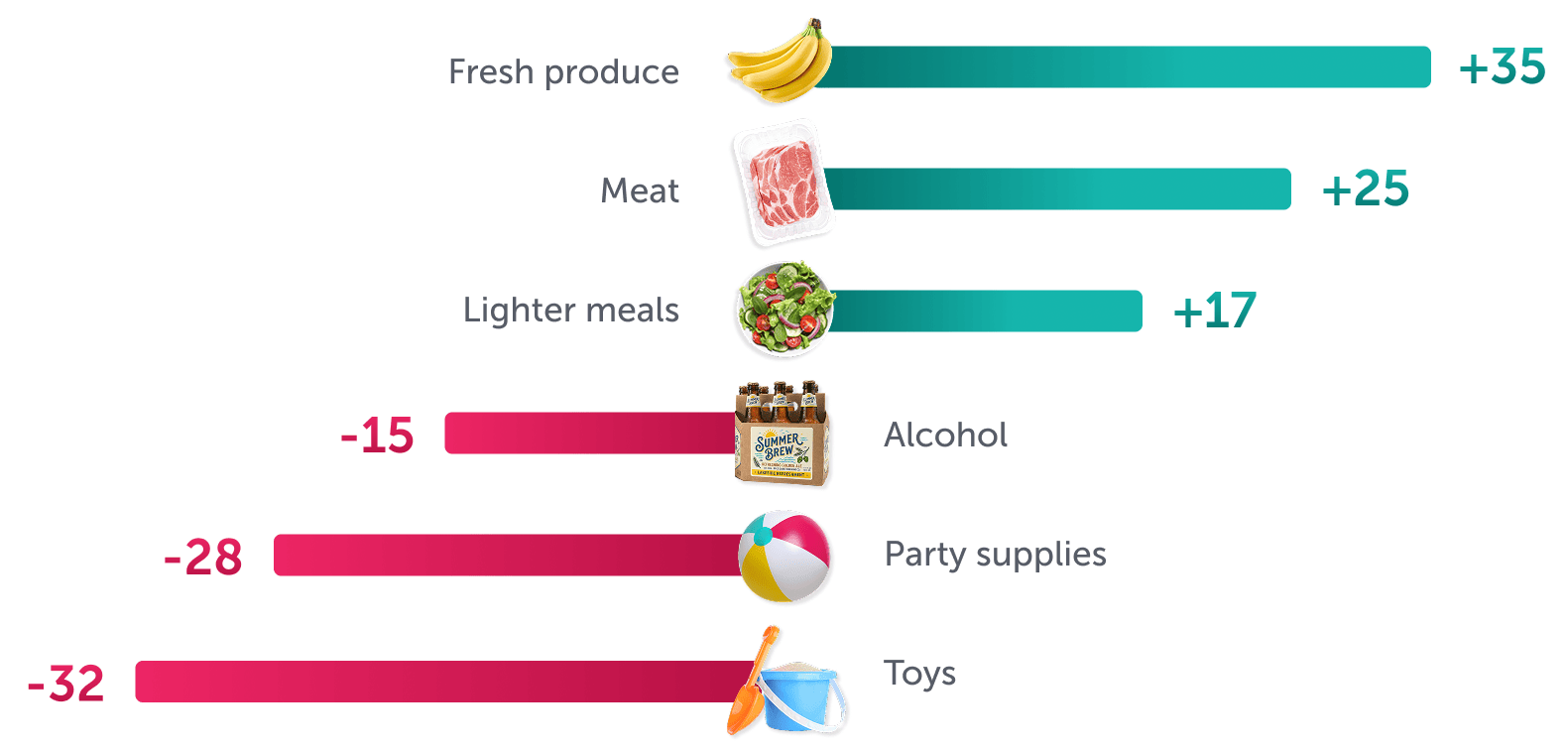

Notably, category data also reflect this shift with fresh produce (+35 net spend intent), meat (+25), and lighter meals (+17) are all expected to gain share, while discretionary categories like toys (-32), party supplies (-28), and alcohol (-15) are losing ground.

This trend suggests that the “summer basket” is being rebuilt around hosting, cooking, and everyday consumption — not travel, novelty, or impulse.

Net spend intent by category heading into summer

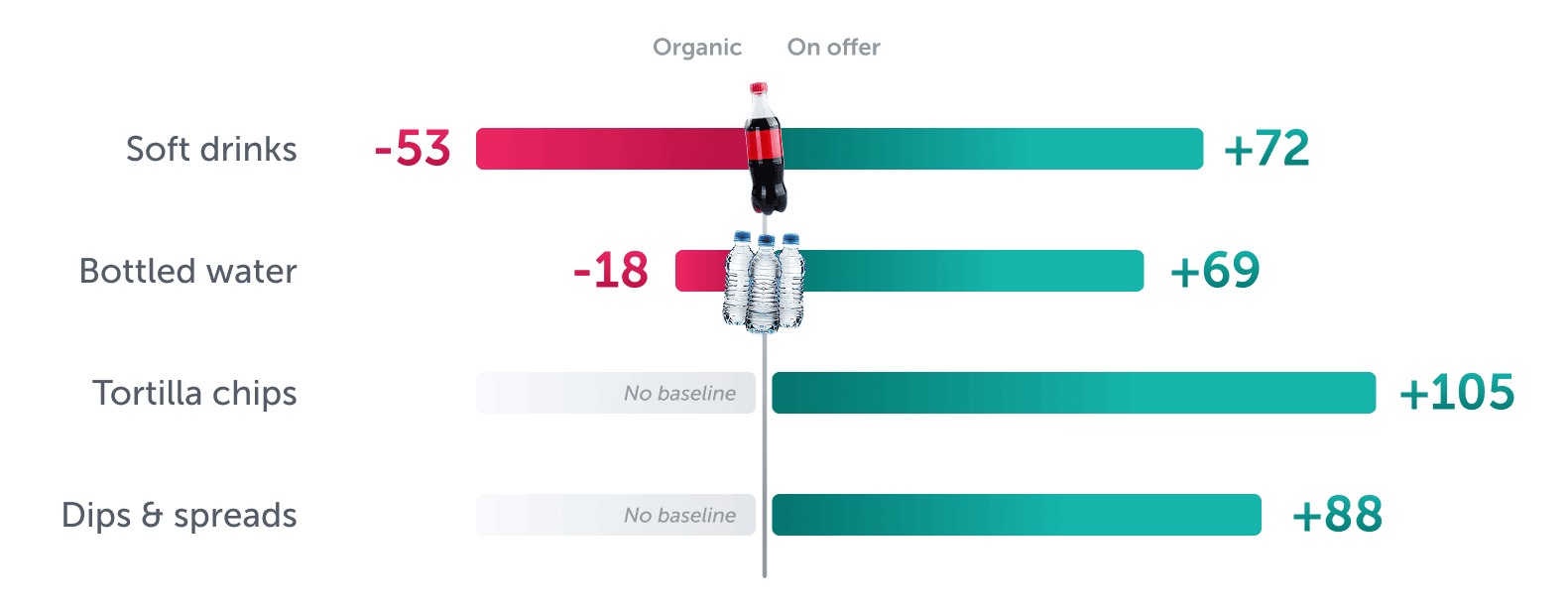

Promotions are outperforming organic demand

In a value-driven environment, promotions are shaping outcomes. Across multiple seasonal moments, promoted categories outperformed their organic baselines.

Without a promotion vs. with one

Demand change by category

As shoppers manage spend more closely, promotions can be a major influence in their purchasing decisions.

That behavior is already visible at scale. Redeemer growth on the Ibotta Performance Network is up 50% from Q4 2023 to Q4 2025, underscoring how actively shoppers are seeking value.

The early signal for brands: Demand is shifting before summer starts

By the time summer officially begins, much of the shift has already happened.

Recent data across retailers shows early acceleration in seasonal categories:

- Sunscreen & tanning: +16.8% weekly growth

- Lawn & garden: +13.1%

- Pest control: +10.9%

Notably, much of this growth is organic, suggesting consumer intent is moving ahead of activation. At the same time, promotional responsiveness in food and beverage categories indicates that when brands do activate, they can meaningfully capture and redirect demand.

What this means for summer 2026

The data suggest that consumers aren’t necessarily spending less across the board, but they’re spending more selectively.

Several patterns are worth watching:

- The basket is being rebalanced: staples hold, discretionary categories soften

- The center of gravity is shifting to the home: Fewer trips, more in-home activity

- Promotions are becoming a decision driver: Value is shaping brand choice

For CPG marketers, timing matters as much as the trend. If these trends continue, the most important demand shifts will occur before the official start of the season, creating an opportunity to align earlier with evolving shopper behavior.